Auto enrolment pensions

The minimum contributions into a workplace pension scheme are not increasing from April 2026. The contribution rates will remain the same for both employees and employers.

Note employees will receive a tax saving equivalent to 1% which reduces their overall cost to 4%.

For the 2026/27 tax year, auto-enrolment qualifying earnings are unchanged, so remain based on gross annual earnings between £6,240 and £50,270 (the Qualifying Earnings Band). Employees aged between 22 and State Pension age (currently 66) earning over £10,000 yearly must be automatically enrolled, with contributions calculated on earnings between £6,240 and £50,270.

It would be worth reminding your employees that if their income exceeds the higher rate tax threshold, they may be able to claim additional relief on their pension contributions.

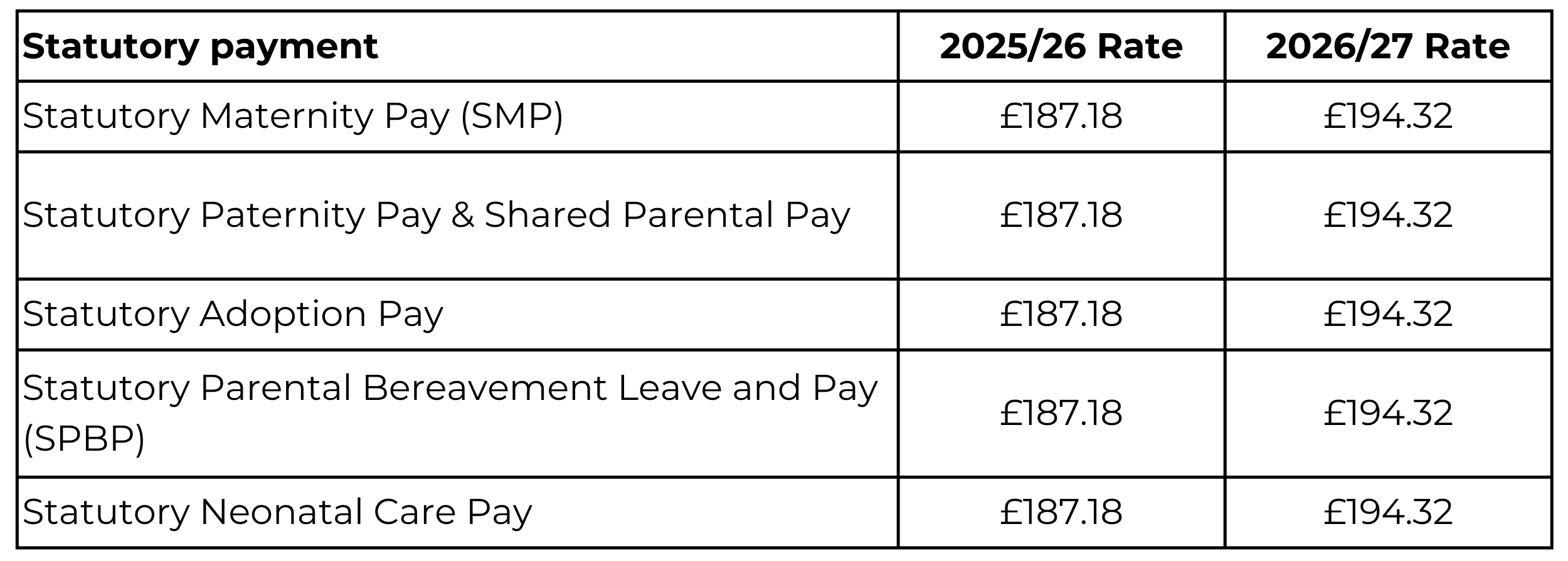

Statutory Payments

Statutory Sick Pay: Under the Employment Rights Act 2025 there have been changes to SSP. The key changes are as follows:

We acknowledge that many employers offer enhanced payments above the statutory limits. It is your responsibility to advise us of any such arrangements.

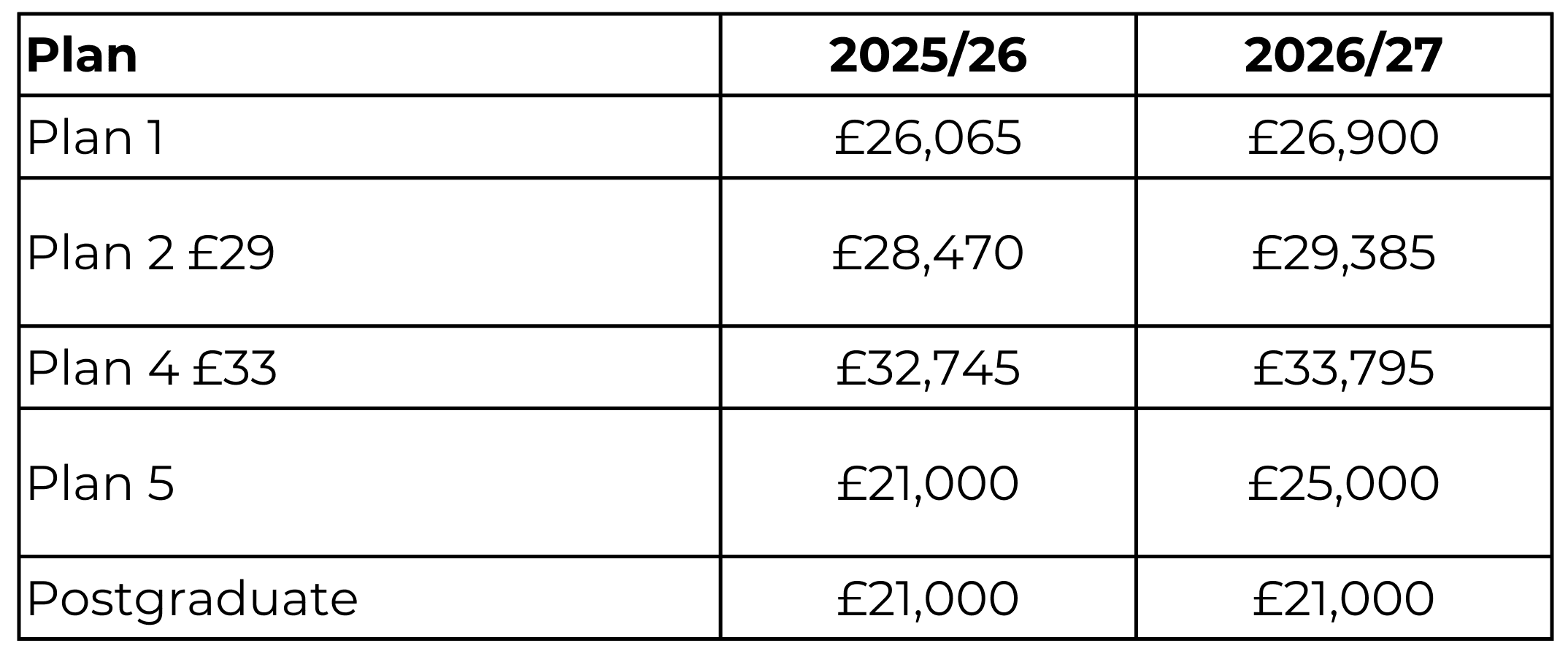

Student & Postgraduate Loans

Please note that the employee thresholds will increase to:

Deduction rates for undergraduate loans (plans 1,2,4 and 5) are 9% of earnings above the threshold. The deduction rate for postgraduate loans remains at 6% of earnings above the threshold.

Student Loans: Off-Payroll Working Rules

When you are processing your payroll, where employment is subject to off-payroll working rules, student loan deductions should not be made. The worker will account for student loan obligations in their own tax return.

CALL US 01325 349700

Join our mailing list today for insights, events and webinars: